Introduction

As the housing market continues to fluctuate, understanding nationwide mortgage rates is essential for potential homebuyers and homeowners looking to refinance. Mortgage rates serve as a critical factor influencing the affordability of homes, making them a significant aspect to consider in today’s economy. Recent trends indicate a rise in rates, prompting many to evaluate their financial strategies regarding home ownership.

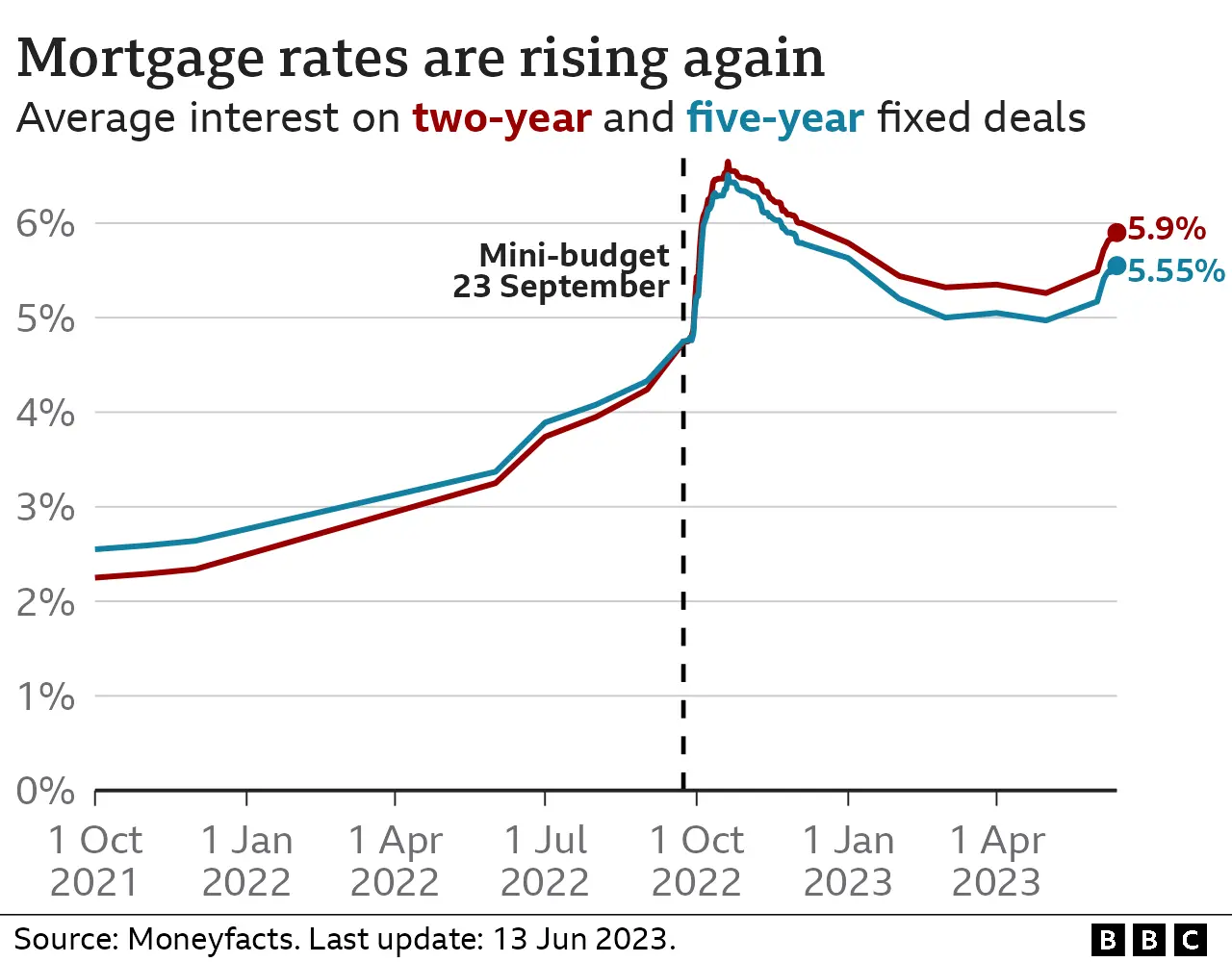

Current Trends in Nationwide Mortgage Rates

According to the latest data from Freddie Mac, the average 30-year fixed mortgage rate in the United Kingdom has surged to 6.77% as of October 2023, a steep increase from the previous year. This upswing can be attributed to a combination of rising inflation and persistent economic uncertainty stemming from global factors, including the ongoing impact of the COVID-19 pandemic and geopolitical tensions. Experts predict that this trend may continue as the Bank of England aims to control inflation through interest rate adjustments.

Factors Influencing Mortgage Rates

Several key factors drive nationwide mortgage rates, including the Bank of England’s base rate, economic growth indicators, and consumer confidence levels. As the central bank raises its rates to combat inflation, lenders often mirror these changes, resulting in higher mortgage rates for consumers. Furthermore, as the economy shows signs of healing, demand for housing may increase, placing additional upward pressure on rates.

The Impact on Homebuyers and Homeowners

The rise in mortgage rates has significant repercussions for both potential homebuyers and existing homeowners. For first-time buyers, higher mortgage rates can limit purchasing power, making homes less affordable and potentially slowing down the homebuying process. On the other hand, homeowners contemplating refinancing may find it less advantageous if they do not secure lower rates than their current mortgage.

Looking Ahead: Future Expectations

Forecasting the trajectory of mortgage rates remains challenging, with many economists suggesting that volatility is likely to persist in the coming months. If inflation continues to rise, it may force the Bank of England to implement further rate hikes, leading to sustained high mortgage rates. Conversely, if economic stability is restored, rates could stabilise or potentially decrease, presenting possible opportunities for homebuyers.

Conclusion

Understanding nationwide mortgage rates is integral for anyone looking to enter the housing market or refinance their property. As circumstances evolve, staying informed about these changes and their implications can empower consumers to make well-informed financial decisions. With a fluctuating economic landscape ahead, monitoring mortgage rates remains crucial in navigating home-buying opportunities effectively.