Introduction to the State Pension

The State Pension is a vital financial support system for millions of retirees in the United Kingdom. As individuals approach retirement age, understanding how the State Pension works and its impact on their financial stability becomes increasingly important. With recent changes in eligibility and amounts, staying informed is crucial for effective retirement planning.

What is the State Pension?

The State Pension is a government-funded payment made to eligible individuals who have reached the State Pension age, which currently stands at 66 for both men and women. It is designed to provide a basic level of financial security in retirement, funded through National Insurance contributions made during the individual’s working life.

Types of State Pension

There are two main types of State Pension in the UK: the Basic State Pension and the New State Pension. The Basic State Pension applies to those who reached retirement age before April 2016, while the New State Pension is applicable to those who reach retirement age on or after that date. As of April 2023, the full New State Pension is £203.85 per week, while the Basic State Pension amounts to £156.20 per week. These amounts are subject to annual reviews and potential increases based on various factors, including inflation.

Eligibility Criteria

To qualify for the State Pension, individuals must have a minimum of 10 qualifying years on their National Insurance record. Full entitlement requires 35 qualifying years. It is essential for workers to regularly check their National Insurance contributions to ensure they meet the criteria for the full State Pension.

Recent Changes and Adjustments

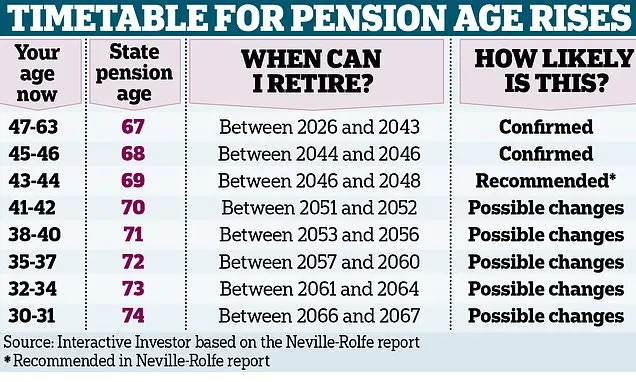

In recent months, the UK government has been evaluating the sustainability of the State Pension system amid rising life expectancy and economic pressures. Proposed changes may include adjustments to the State Pension age, with discussions suggesting a potential increase to 67 by 2028. Furthermore, the government is reviewing the link between pension increases and earnings growth, inflation, or a combination of both.

Conclusion and Implications

The State Pension remains an essential element of retirement planning for many in the UK. Understanding its structure, eligibility, and potential changes is crucial for current and future retirees. As discussions around pension reforms continue, it is prudent for individuals to stay informed and consider complementing their State Pension with private savings and investments. By doing so, they can ensure a more secure financial future in retirement.