Introduction

The Lifetime Individual Savings Account (Lifetime ISA) is an innovative savings scheme designed to help individuals in the UK save for their first home or for retirement. Introduced in 2017, the Lifetime ISA has gained popularity, especially among younger savers, due to its unique benefits, including government bonuses and flexible withdrawal options. Understanding the mechanics of a Lifetime ISA is crucial for anyone considering it as a savings strategy for future needs.

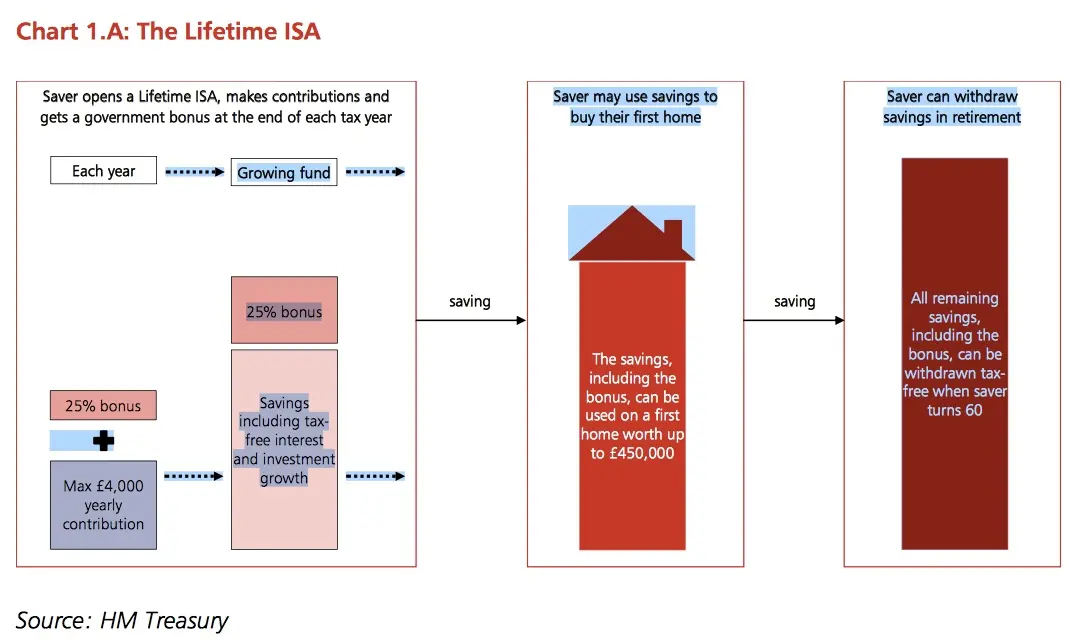

Key Features of the Lifetime ISA

The Lifetime ISA permits individuals to save up to £4,000 each tax year, with the government adding a 25% bonus on contributions made. This means that for every £1 saved, the government will contribute an additional 25p, capped at a bonus of £1,000 per year. Importantly, this scheme is open to individuals aged 18 to 39, promoting early saving habits among younger generations.

Funds contributed can be used to assist in purchasing a first home worth up to £450,000 or to provide a supplementary income in retirement after the age of 60. One of the standout features is the ability to withdraw funds tax-free, making it an attractive option for both homebuyers and retirees.

Current Trends and Events

As of late 2023, the Lifetime ISA continues to be a focal point for government discussions on savings initiatives amidst rising housing costs. With an increase in house prices, many young people face challenges in entering the property market. The government has reiterated its commitment to supporting first-time buyers through this savings scheme. Furthermore, recent surveys indicate an increased uptake of Lifetime ISAs as potential savers recognise the importance of tailored savings plans.

Financial experts are urging potential savers to explore Lifetime ISAs thoroughly. While they offer substantial advantages, there are restrictions; for example, if the funds are withdrawn for reasons other than buying a first home or after turning 60, a 25% penalty is applied to the savings. This aspect necessitates careful planning and understanding of individual financial goals.

Conclusion

In conclusion, the Lifetime ISA presents a viable option for young individuals aiming to save for their first home or to establish a sound retirement fund. With benefits such as government bonuses and tax-free withdrawals, it stands out as a financial tool fostering proactive savings. However, as with any financial product, it is essential for individuals to weigh the pros and cons, considering their financial situations and future aspirations. The Lifetim ISA’s role in the UK savings landscape remains vital, particularly for a generation facing challenges in home ownership and retirement planning.