Introduction

The Bank of England base rate is a crucial economic indicator that affects everything from mortgage costs to consumer spending. Recently, changes to this interest rate have become an important topic of discussion, especially as the UK grapples with increasing inflation and economic uncertainty. Monitoring the rate is vital for both individuals and businesses, as it influences borrowing costs and saving returns.

Recent Developments

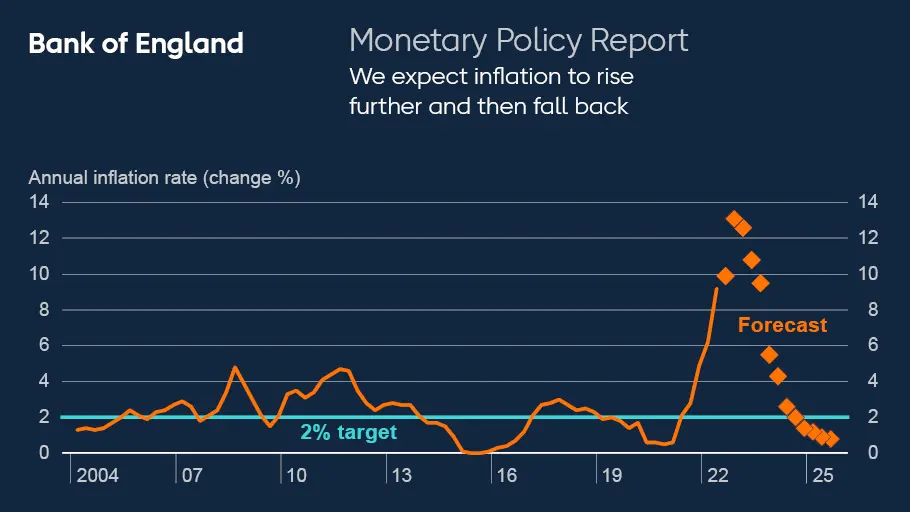

As of October 2023, the Bank of England has set the base rate at 5.5%, unchanged since its last adjustment in September, when it was raised to combat rising inflation. This decision followed a series of increases over the past two years aimed at curbing the inflation rate, which reached a peak of 11.1% in late 2022. The bank’s Monetary Policy Committee (MPC) is tasked with maintaining inflation at around 2%, and maintaining the base rate is a tool they use to influence inflation and support economic stability.

The recent decision to hold the rate steady reflects a cautious approach by the Bank. Analysts and economists had anticipated this move amid signs of easing inflationary pressures and a potential slowdown in economic growth. A survey from the Confederation of British Industry indicated a decline in retail sales growth as consumer confidence wanes. With potential recession concerns looming, the Bank aims to balance these economic factors while discouraging inflation from spiralling out of control.

Impact on the Economy

The base rate has a direct influence on the cost of borrowing and the return on savings. When rates are high, it typically leads to increased mortgage payments and loan interest, which can dampen consumer spending. Consequently, businesses may experience decreased demand for goods and services. On the other hand, higher savings rates can encourage consumers to save more, potentially offsetting some negative impacts on spending.

Market experts suggest that if inflation continues to decline, the bank may look towards a potential decrease in the base rate early next year. However, any such reduction would depend greatly on the economic climate and inflation trends as they unfold. The next MPC meeting scheduled for November 2023 will be critical in indicating the Bank’s future outlook.

Conclusion

The Bank of England base rate remains a vital tool for managing the UK economy in uncertain times. With ongoing inflation pressures and indications of softer consumer demand, stakeholders from homeowners to business owners must stay informed about potential changes to the rate. As the economic landscape evolves, the implications of these decisions by the Bank will be felt across the country’s financial system, making it increasingly important for individuals and enterprises alike to keep abreast of developments in the base rate policy.